Blog

Tarun Sridhar

Matt Gamser

Member Pulse Survey #2 on the Impact of COVID-19 - May

One of the most important aspects of any crisis is the ability to adjust quickly to the situation. The SME Finance Forum team sent out a survey to its members in April to assess how their institutions and their SME clients are coping so far with the disruptions. One month on, we shared an update of the initial pulse survey. Members continue to be quite responsive, given all the distractions, with 54 institutions responding this time, compared to 45 in April (out of a possible 137).

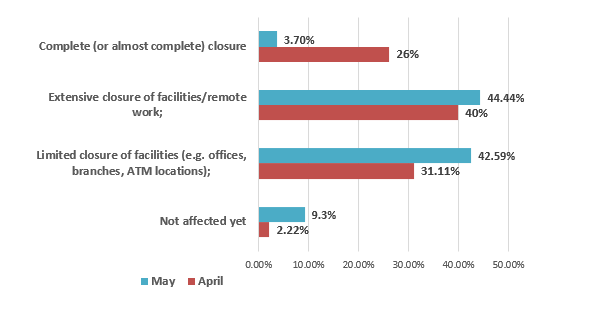

We are starting to see some opening up in some markets, with significantly fewer in the complete closure response, (less than four percent versus 26 percent in April), and more reporting business close to usual (nine percent, versus only two percent in April).

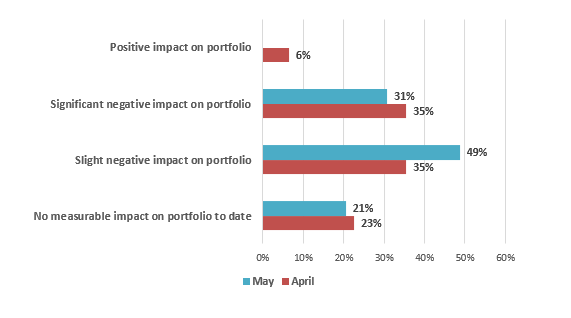

However, 72 percent of respondents report moderate or severe adjustments to their operations due to COVID-19. Fewer are citing liquidity challenges, and declines in sales revenue, but there’s been a moderate uptick in reports that assets are impaired (up to 30+ from 20 percent in April) – so short term liquidity problems may have been resolved, but longer-term business problems may be looming.

There is increasing confidence that government interventions will help their businesses and slightly lesser for their clients. While more lenders see declines in portfolio quality, fewer report significant declines than last month. Also, a higher percentage reports doing new lending, not only to existing customers, but also to new clients, and the tightening of credit criteria appears to have peaked.

The vast majority still have much of their portfolio under moratoria or other deferrals of 1-6 months. Nonetheless, a majority feels they’ll have the same or higher revenue, customers, and lending activity this month (compared to a small minority in April). So, this might point to growing confidence in the ability of members to rebound quickly as economies reopen.

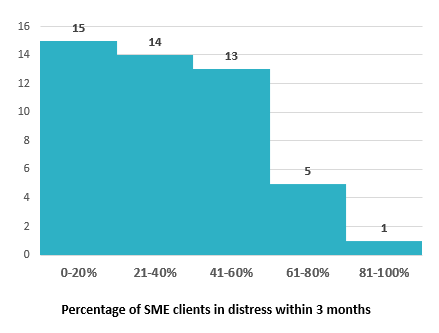

This confidence extends to customers. In April, most members felt the majority of SME clients would be in severe financial distress in the next three months. This month, most members think the majority of SME customers will not be in distress over the same future period.

Cause for hope all around, or wishful thinking coming from work from home confinement?

Tune in next month, when the reopening of commerce is farther along, and we will see!