Blog

Tarun Sridhar

Matt Gamser

Member Pulse Survey #5 on the Impact of COVID-19 - August

Aug 20, 2020

Some improvements reported but overall, members remain wary…

This month’s pulse survey received 56 responses.

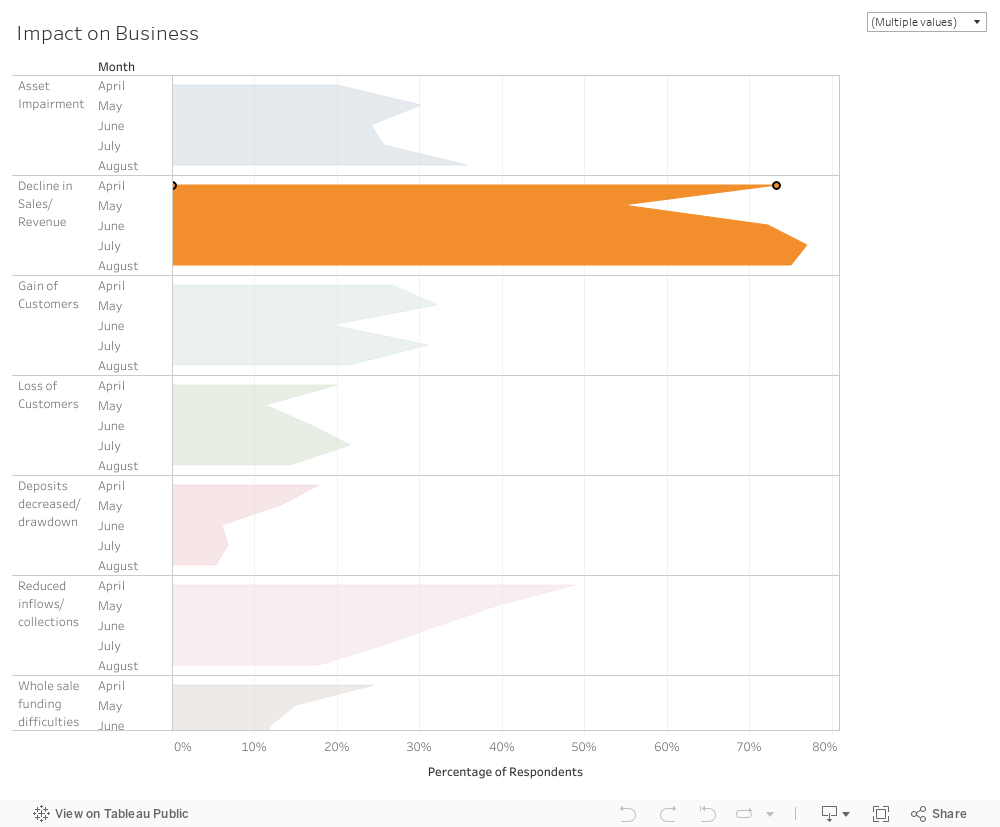

Our members are showing signs of improvement, with the exception of a 10-percentage point increase in Asset Impairment. We see a similar trend among the consistent respondent sample (June-August).

More members are reporting that they are affected by limited closure. Among the consistent respondent members, we see a 11-percentage point increase in members ‘not affected’ by closure (70% are affected by limited closure or no closure).

More members reported that government responses were causing problems for their business (18 percentage point increase). The consistent respondent sample does not concur as we see only a marginal increase reported. In addition to this, lesser members are reporting that government responses are likely to help their clients.

Portfolios still seem largely affected. 81% reported at least a slight or significant impact on their portfolio. The consistent respondent sample provides us with a relatively more optimistic view of our members’ portfolio quality - we see a 15-percentage point increase in members saying there is no measurable impact. However, 72% of this sample still report a slight or significant impact on portfolio

In relation to lending, the results show a 13-percentage point increase in members reporting lending to new customers and a 23-percentage point increase in the consistent respondent sample for the same.

More members have reported they are issuing Blanket moratoria (voluntary and mandatory). The consistent respondent sample shares the same trend.

Looking ahead, 91% of our members who responded expect to have about the same or more customers next month (90% among consistent respondents) and 80% expect to have the same or more revenue next month (69% among consistent respondents). While lesser members expect to lend more next month (-9 percentage point), 83% (negligible change since July) expect to lend more or lend at the same levels. This result is still a good sign because we saw a sharp increase in members lending to new customers.

Almost 50% of our respondents expect 0-20% of their SME clients to be in financial distress in three months (7-percentage point increase since July). While our members’ perception of their SME clients’ health gets better every month, we must be cognizant of the other side of the coin - 51% (54% of the consistent respondent sample) still expect more than 21% of their SME clients to be in financial distress in three months.

Our swift action to launch a COVID-19 pulse survey right from the onset of the global pandemic, with the help of our members, has allowed us to now visualize some form of a recovery. Lesser members are facing liquidity challenges, more members are lending to new customers, more members are feeling optimistic about their business and SME clients. But not all data points are pointing to a recovery path. Majority of members still report decline in sales, we’re also seeing an increase in members reporting asset impairment, the health of member’s portfolio has not changed much, and more are tightening their credit criteria.

It is apparent, through the data, that there is an acknowledgement of the resiliency and adaptability of SMEs so far——but we have a long way still to go

Let us know what insights you can derive from the data.

Read full report here>